AWS Vs. Microsoft Vs. Google: How Partners Rank The Big 3 Cloud Companies

CRN’s exclusive Cloud Barometer survey asked solution providers to divulge the biggest pros and cons of the three top platforms. Here are the results, and why it’s anyone’s game to win.

One of the earliest and most accomplished solution providers focused on Amazon Web Services, 2nd Watch spent seven years as a single-cloud shop: shifting workloads to more than 100,000 AWS instances, providing managed cloud services and helping propel the platform to its commanding lead in the market.

Then, in late 2018, a large customer came to the solution provider with a problem. Along with running AWS, the consumer-facing brand also operated an environment on Microsoft’s cloud platform, Azure. And managing workloads consistently across both clouds, in a single way, had become a struggle.

As it turned out, this customer wasn’t alone. With multi-cloud management needs becoming widespread, 2nd Watch launched an Azure practice and added Microsoft Gold partner status to its credentials, alongside its AWS Premier partner status.

“It was really driven by our customers,” said Chris Garvey, executive vice president of cloud services at Seattle-based 2nd Watch, speaking of the company’s expansion beyond AWS.

And then, a third cloud entered the picture. Amid increased demand for Google Cloud, 2nd Watch went on to launch a practice for that platform in May 2020.

“We have a deep partnership with AWS. We always will,” Garvey said. “But ultimately, in the same way that AWS focuses on its customers first, we take the same approach.”

The journey at 2nd Watch mirrors the evolution of the cloud Infrastructure-as-a-Service market itself—which has gone from early dominance by pioneer AWS to become a hard-fought, three-way race between tech giants Amazon, Microsoft and Google.

As solution providers look to place their next bets in the cloud infrastructure services market—which Synergy Research Group pegged at nearly $130 billion last year—a new CRN survey and interviews with top cloud solution providers reveal some of the biggest strengths and weaknesses of each platform.

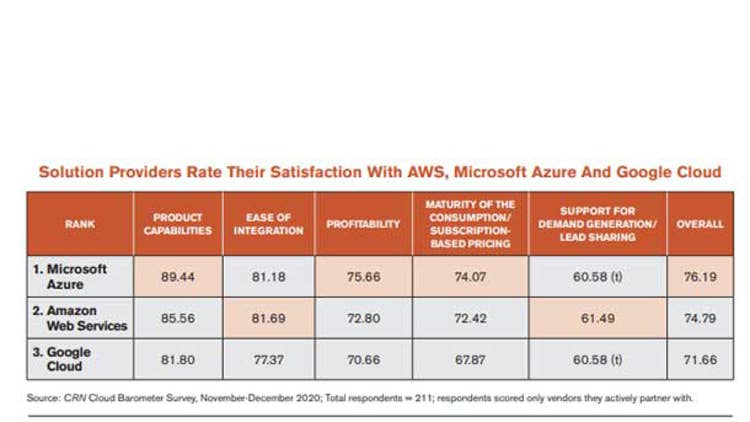

CRN’s Cloud Barometer survey asked solution providers to rate their satisfaction with the three leading cloud platforms across five key categories listed here in order of importance to them—product capabilities, ease of integration, profitability, maturity of pricing, and support for demand generation and lead sharing (see results below). The survey received responses from more than 200 solution providers, all of them sellers of cloud IaaS services, who were invited to rate the platform providers they currently partner with.

Survey respondents awarded Microsoft Azure with the highest overall satisfaction rating—giving it first-place finishes in product capabilities, profitability and maturity of pricing.

Meanwhile, AWS ranked No. 2 overall, winning the highest ratings in ease of integration and support for demand generation. Google Cloud, ranked No. 3 in the survey, garnered no first-place finishes.

There’s a good reason that Microsoft edged out its rivals in the survey results, according to Reed Wiedower, global alliances leader and CTO for the Cognizant Microsoft Business Group, a Microsoft Gold partner and Azure Expert MSP.

“Their partner programs are much more mature,” Wiedower said. “Microsoft has just been in the business of partners for much longer than Amazon or Google.”

A higher percentage of Azure solution providers responding to the survey—58 percent—said they felt they had a highly strategic sales relationship with Microsoft over the previous three months, taking into consideration elements such as conducting joint sales calls, mutual account planning, sharing customer insight and general sales teaming to grow the business. That compares with 43 percent of AWS partners and 31 percent of Google Cloud partners who felt they had a highly strategic sales relationship with the respective vendors.

More Microsoft Azure solution providers responding to the survey also said they expect high levels of cloud IaaS growth with the vendor over the next 12 months, with 65 percent saying they expect double-digit growth. Fifty-four percent of responding AWS partners said they expect double-digit cloud growth with the vendor, while for Google Cloud it was 44 percent of partners.

Microsoft Channel Chief Rodney Clark said that partners have long been at the center of how the company delivers technologies to customers. “We view this ranking as an affirmation of our commitment to provide opportunity for partners to build and sell differentiated solutions that help customers migrate to the cloud,” Clark said in a statement provided to CRN. Representatives from AWS and Google Cloud declined to comment.

While survey respondents gave Microsoft the No. 1 ranking in the inaugural CRN Cloud Barometer survey, the margin of victory over AWS was slim. The survey also revealed that third-ranking Google Cloud is picking up new partners at a rapid clip—and is not far behind the other two platforms in terms of overall partner satisfaction. For the foreseeable future, the clash of the cloud titans is shaping up to be a fierce battle in the channel.

Cloud Surge

All three vendors are investing heavily in their cloud platforms, from product updates to channel program enhancements. In the IaaS market of 2021, “competition is indeed intense,” said John Dinsdale, a chief analyst at Synergy.

As of the first quarter of the year, AWS maintained its lead with a 32 percent share of enterprise spending in the cloud infrastructure services market, according to Synergy. AWS’ market share has stayed essentially flat—hovering between 32 percent and 34 percent—for the past four years, Synergy reported.

By contrast, Microsoft Azure has leapt from an 11 percent share of the market four years ago to 20 percent market share today, the research firm said. And Google Cloud now has a 9 percent share of the market, up from 6 percent four years ago, according to Synergy.

Already one of the most lucrative professional and managed services opportunities for partners, the cloud has surged due to widespread business uncertainty and the need to enable remote work during the COVID-19 pandemic. Enterprise spending for cloud infrastructure services reached $39.5 billion during the first quarter of 2021, a 37 percent spike from the same period a year earlier and up $2 billion from the prior quarter, Synergy reported.

For the three biggest cloud infrastructure platforms, offering a unique value proposition is as crucial as ever, said Sid Nag, research vice president at Gartner.

The fact that multi-cloud deployments are increasing is “all the more reason they need to differentiate,” Nag said. “It puts pressure on the individual cloud providers to be best-in-class in everything.”

In interviews with CRN, executives at cloud solution providers detailed the biggest pros and cons they see with Azure, AWS and Google Cloud across the five categories of the survey.

Microsoft Azure: Leader In Product, Profits And Pricing

In the survey, product capabilities ranked as the most important category for partners—and Microsoft’s Azure platform received the highest satisfaction rating there.

Azure is a natural fit for many customers due to the widespread use of Microsoft’s other cloud platforms—Microsoft 365, which includes Outlook and Teams, and Dynamics 365 for CRM and ERP, according to solution providers.

“Because it’s part of the Microsoft organization, Azure already has an immediate relevance with many of our customers,” said Bob Bailkoski, CEO of global solution provider Logicalis Group, a Microsoft Gold partner and Azure Expert MSP. “There’s a natural affinity.”

While Logicalis is also an AWS Consulting partner, the company does significantly more work with Azure than AWS, Bailkoski said—and the Azure business at Logicalis saw triple-digit revenue growth during the company’s fiscal year that ended in February.

“Microsoft’s articulation of the opportunity that’s available with Azure is much easier for our customers to understand—especially in the C-suite—than it is perhaps with AWS, which is a slightly more technical, developer-style solution,” he said.

Azure benefits hugely from the fact that Microsoft 365 users already have identities in the cloud platform via the Azure Active Directory authentication service, solution providers said.

While it’s possible to extend Active Directory into AWS, “you don’t get Azure AD,” said Zach Saltzman, senior director for the Microsoft platform at FMT Consultants, a Microsoft Gold partner based in Carlsbad, Calif. “And Azure AD is this whole separate beast that brings a lot of productivity features and a lot of security features that no other cloud has.”

The biggest differentiator for Azure is its connection to Microsoft’s other two clouds, Microsoft 365 and Dynamics 365, Saltzman said.

“It’s like a cloud mesh,” he said. “Microsoft is able to drive these synergies between their three clouds that AWS and Google Cloud just can’t.”

Those synergies are possible because Microsoft is a software company at heart, said Michael Spoont, president of ProArch, an Atlanta-based Microsoft Gold partner.

“AWS was not a software business—they came into the software business to enable them to better manage their product business. But they’ve never built business solutions. They’ve never built applications. They’ve got an operating environment. But there’s no Dynamics equivalent in AWS, for example,” he said.

And if you use Dynamics 365 or Microsoft 365, you’re already using Azure, Spoont noted. The many points of entry into Azure for Microsoft customers “does separate Azure from the other cloud providers,” he said.

Supporting hybrid cloud infrastructure is another strength for Microsoft, which embraced hybrid cloud earlier than AWS, Microsoft-focused solution providers said.

“Microsoft created the gold standard in terms of operating in a hybrid environment,” Spoont said.

With offerings such as Azure Stack, Microsoft enables customers to leverage their investment in their on-premises environment and fully integrate it with their cloud environment, he said.

Azure Stack was the “holy grail” for hybrid infrastructure when it first launched several years ago, said Jon Thomsen, CEO of Beaverton, Ore.-based Atmosera, a Microsoft Gold partner and Azure Expert MSP.

“It’s a key differentiator,” he said. “Azure makes [hybrid] really easy with Azure Stack. Then there’s Azure Stack Edge for storage and AI gateways, Azure IoT Edge for IoT devices, Azure Arc for centralized management and deployment of on-premises infrastructure as well as in the cloud. Microsoft is committed to that hybrid environment.”

One of the newer unique Azure capabilities is Windows Virtual Desktop, which enables multiple users to connect to Windows 10 virtual desktops on a single virtual machine. The offering has been seeing soaring demand as a way to enable the remote workforce.

The pre-existing integration for WVD with Azure Active Directory “means that I can spin that up a heck of a lot faster than I can otherwise,” said Mike Wilson, vice president and CTO of Interlink Cloud Advisors, a Microsoft Gold partner based in Mason, Ohio.

“I can do that because Microsoft already has the user identity,” Wilson said. “It’s not that you couldn’t go do something similar in AWS, but they don’t have the same infrastructure that customers already have in place on the Microsoft platform.”

The other categories where partners rated Azure No. 1 in the survey were on profitability and maturity of pricing.

For FMT Consultants, Saltzman said, the profitability of Azure has always been a strength. There may not be substantial margin in licenses—it’s typically about 15 percent—but there are a number of accelerators and additional rebates available, he said. These additional incentives can add another 9 percent, Saltzman said.

“At the end of the day, it’s recurring revenue. And even if the margin is small, it’s very attractive,” he said.

Many existing Microsoft customers also find pricing advantages in sticking with Azure when migrating to cloud infrastructure, solution providers told CRN.

For instance, while prices for Azure and AWS are generally similar, Microsoft’s Azure Hybrid Benefit has made Windows Server and SQL Server workloads far more affordable to run on Azure, Wilson said.

“When you’ve already made an investment in Microsoft licensing, you can now transition that and bring that to Azure in a way that you can’t do with AWS,” he said.

In looking at the way that offerings from AWS and Azure are marketed, they can sound very similar, said George Burns, senior consultant for cloud operations at SPR, an AWS Advanced Consulting partner and Microsoft Gold partner based in Chicago. “But in execution they’re very different,” he said.

The AWS approach, Burns said, is to present all possible components to the user. “AWS is really good at exposing everything to the developer,” he said. But for Microsoft, whose roots are in the Windows operating system, guiding users visually is more its forté, he said. With Azure, Microsoft presents a computing solution that tends to be more user-friendly, Burns said.

“Microsoft has a look and a feel that people are very comfortable with,” he said.

Ultimately, when you invest in the Microsoft ecosystem, “it generally serves you well in your investment if you keep buying into the Microsoft ecosystem,” Burns said. “It’s a great model and it rolls together well. But it really works best for those that buy all in.”

AWS: Leader In Ease Of Integration And Demand Generation

In the Cloud Barometer survey, partners ranked ease of integration as the second most-important category—and for that category, AWS received the survey’s highest rating.

That ties back to AWS’ emphasis on providing users with a comprehensive set of components, Burns said. Whereas Microsoft positions its offerings as packaged solutions, “AWS positions all of their offerings well for integration,” he said.

At 2nd Watch, which began working with AWS in 2011, Garvey agreed that the cloud platform excels when it comes to providing users with the full spectrum of services.

“I think AWS has done a great job at providing a large suite of services that are tailored to specific types of transformation needs,” he said.

One example is database modernization, for which AWS offers “many different services that cater to different patterns of data usage, and that are driving a pretty strong integration scenario,” Garvey said.

In general, AWS takes a “builder-first” approach in its offerings, he said. “From a development and engineering standpoint, they cater well to traditional full-stack engineers,” Garvey said.

AWS’ greater scale also offers an advantage over competing clouds in numerous ways, AWS-focused solution providers told CRN.

“With scale comes experience, knowledge, perfection of product and services,” said Eran Gil, CEO of San Francisco-based AllCloud, an AWS Premier Consulting partner. “At scale, you get to a much better product.”

That scale has come into play on projects that AllCloud has worked on, including one to move BMC’s Control-M on-premises application into AWS so that it could be offered as a service, he said.

Thanks to its scale and experience, AWS has built an entire organization around the capability of “SaaS-ifying” ISV products, Gil said. The organization, AWS SaaS Factory, worked with AllCloud to take BMC’s on-premises application and turn it into a multitenant SaaS product.

“It does take scale to get to build such nuanced teams, which adds so much value,” Gil said. “AWS’ premise is to go and help companies become more native to the cloud. And through scale, they have the experience, knowledge and capability to guide [customers] through that rather long journey.”

Amazon’s greater scale also makes a difference in terms of ensuring that capacity is available, said Josh Quint, senior director of cloud solutions at ServerCentral Turing Group, an AWS Advanced Consulting partner based in Chicago.

For instance, AWS encourages users to buy reserve capacity and has never experienced issues with providing it, Quint said. Microsoft, however, does not offer any guarantees on Azure capacity and actually faced capacity constraints early on in the pandemic, as well as outages in March 2020 caused by strains placed on some of its cloud services.

“I’ve never run into an issue where I can’t spin up [AWS] resources. We’ve never had an inkling of capacity issues. And performance or ‘noisy neighbor’ issues—I’ve just never really seen it,” he said. “Whereas this last year, [Microsoft] just got hammered by everybody deciding to move into Azure during COVID, and starting to use [Microsoft] 365 and Teams. There were definitely some physical capacity issues there.”

In terms of partner engagement, Quint said that AWS has taken the approach of interacting directly with his company and providing guidance—even when it was a small outfit.

That’s because AWS still brings a startup mentality and has a fondness for “the small and scrappy,” he said.

“Even when we were tiny, we had a rep. We had somebody that was going to come in and guide us through the process,” Quint said. “Not so much with Microsoft. You have to be a certain size to get that personal touch. It was like pulling teeth to try to figure out where to even start. The best way you could start is to just hire somebody that’s done it, but that’s not easy to do either. AWS will guide you to a certain extent.”

AWS’ inclination toward engaging directly with the channel has also led to a greater propensity for supporting demand generation, according to solution providers. Partners rated AWS the highest in the survey in support for demand generation and lead sharing.

Andover, Mass.-based Navisite is an AWS Advanced Consulting partner as well as a Microsoft Gold partner and Azure Expert MSP, and has seen the difference in how the two companies engage with partners around customer prospects, said CEO Mark Clayman. AWS gets far more involved with providing leads than Microsoft, Clayman said.

At AWS, “they obviously have a very large sales force, but their partner engagement model is as large as their direct sales force. And once they find a customer that is the right fit for the AWS platform, what they tend to do is go out and find the right partners to engage with them and then help that customer,” Clayman said. “There’s a good relationship between AWS and the partner community to solve that need for that customer.”

Microsoft gravitates more toward leveraging its pre-existing relationships with customers to build momentum with those migrating to Azure, he said. Microsoft has “a lot of good programs, and they have funding, and they want to enable you—but they’re not quite as effective on the street, working directly with our reps and their partner reps,” Clayman said.

By contrast, AWS brings “a very good partner-enabled model,” he said. “And I think really where that came from is AWS was really starting from scratch—they had no existing relationships with customers when they started their platform. So I think that they made a smart move and they started with a partner ecosystem from the beginning.”

Google Cloud: Engaging With More Partners

Solution providers ranked Google Cloud No. 3 overall in the Cloud Barometer survey, giving it a third-place finish in all categories except one.

However, it is rapidly expanding its partner ranks, extending its enterprise reach. According to data provided by Google Cloud, the vendor’s channel partner community has grown by more than 400 percent over the past two years. That influx of new partners is reflected in the survey, where 43 percent of Google Cloud solution providers said they have been working with the vendor for less than two years. That compares with 35 percent of AWS partners and 23 percent of Microsoft Azure partners working with those vendors respectively.

Along with bringing aboard top cloud partners such as 2nd Watch, Google Cloud has also added leading solution providers such as Navisite and Chicago-based AHEAD over the past year.

“As the industry continues to mature, we’re seeing a growing demand for Google Cloud in some of our enterprise accounts,” said Stephen Ayoub, president of AHEAD, which is also an AWS Premier Consulting partner and Microsoft Gold partner. “AHEAD is dedicated to partnering with the best-in-breed technology, and we felt it was important to invest in this relationship.”

In the past two years—since the hire of Thomas Kurian as Google Cloud CEO—the platform has been branching out beyond its initial focus on the developer community, solution providers said.

Navisite joined the Google Cloud partner program in March, partly in response to Google’s move to build a go-to-market model that’s more along the lines of AWS, Clayman said.

“They’ve been starting to hire and build out a traditional enterprise sales force,” he said.

Notably, in the Cloud Barometer survey, Google Cloud tied for second place with Microsoft Azure in the category of support for demand generation and lead sharing, its best showing.

“The feeling and the culture that [Google Cloud has] been developing is that they want to share leads,” Clayman said. “They want to have their reps out on the street—finding a new customer and then sharing that customer relationship or that opportunity with their partner community.”

In 2020, partners were involved in three times more customer deals for Google Cloud than in 2018, according to information provided by the vendor—while the number of enterprise customer accounts with a partner attached increased by 50 percent between 2019 and 2020.

SADA Systems, the Google Cloud Reseller Partner of the Year for 2018 and 2019, has seen a “big shift” over the past two years with Google Cloud being included on RFPs that it never was before, said CEO Tony Safoian.

“We’re always given the RFP now. We’re always in the mix,” he said.

Part of Google’s growing appeal derives from its development of key open-source technologies that underpin multi-cloud and hybrid cloud approaches, such as Kubernetes container orchestration and the Anthos “Kubernetes anywhere” platform, according to several Google Cloud-focused solution providers.

And while those technologies are designed to be deployed on any infrastructure—including competing clouds—Google Cloud offers the best-engineered and most cost-effective solution for running them, the solution providers said.

Google Cloud, Safoian said, “invented the standards in which multi-cloud and hybrid cloud exist. I think AWS didn’t say the word ‘multi-cloud’ until last year.”

Los Angeles-based SADA sold its Microsoft practice in early 2019 to focus entirely on Google Cloud—even though the solution provider had won multiple Microsoft Partner of the Year awards over the years.

“We just believe Google’s strategy is the most evolved, most pro-customer, most operationalized—and that it best reflects the market reality,” Safoian said.

On the whole, Google Cloud’s biggest differentiator is its approach around tapping into technologies honed through massive products such as Gmail, the Google search engine and YouTube, said Rajesh Abhyankar, CEO of Princeton, N.J.-based MediaAgility.

“That includes all the developer tools and all the DevOps capabilities—automation of infrastructure, Kubernetes, Anthos and the AI stack,” Abhyankar said. “Google is sitting on so much data because of their free products that their AI capability is way above anyone else.”

MediaAgility—which holds Google Cloud specializations including infrastructure, application development and machine learning—has used Google Cloud capabilities to rapidly increase the processing of data for scientists in biotech labs, for instance. Projects have included reducing the data processing times for genome sequencing experiments from a day to less than an hour using Google Cloud, Abhyankar said.

“The big difference is that Google has been building planet-scale applications—applications for a billion or 2 billion users,” he said. “And the infrastructure needs for those applications are what is baked into Google Cloud’s product.”

Google Cloud’s rankings from partners in the Cloud Barometer survey reflect the fact that some amount of maturing is still needed in the Google Cloud ecosystem, said Allen Falcon, CEO of Cumulus Global, a Westborough, Mass.-based Google Cloud partner.

While the AI and machine learning capabilities offered by Google Cloud are among the best out there, the platform’s two big rivals each have a more mature ecosystem, he said.

For Azure in particular, “you’ve got more tools, both from Microsoft and from third parties. And you’ve got a broader range of partners in the community that are doing more with those tools,” said Falcon, whose company is also a Microsoft Silver partner. “Google has made some great strides in the last 12 to 18 months. But I still see the Microsoft ecosystem as a bit more mature. And clearly AWS is a very mature ecosystem.”

For the Google Cloud ecosystem to reach the same level, “it’s going to take time,” he said. “But Google also might need to assess what they could do to accelerate that time frame.”

Along with continuing to add partners, Google Cloud might want to invest in helping more companies to provide partners with development services related to the platform, Falcon said.

“If there were more firms focused on [providing these services] to other partners, then you’d see greater adoption,” he said.

Ultimately, all three of the cloud platforms are positioned to see huge growth in 2021 and beyond, according to solution providers.

While agility and scalability have always been among the biggest selling points for cloud, the pandemic has made those capabilities a business imperative for more customers, solution providers said.

“For a company like us, it’s been an opportunity to really get people to listen to what we’ve been trying to tell them for the last few years,” said Rosalyn Arntzen, CEO of Redmond, Wash.-based solution provider Amaxra.

The Microsoft Gold partner doubled its cloud revenue in 2020, year over year, and expects to do the same this year. “I don’t think it’s slowing down,” Arntzen said.